SaaS Companies: Is it Investor’s First Love??

The estimation of SaaS organizations is much more than software product sales organizations. Public SaaS organizations have a Revenue median ratio to Enterprise of 6.6x compared with 3.0x for software organizations according to Software Equity Group. Do Investors adore SaaS companies as they have higher valuations or do SaaS organizations have higher valuations as Investors loves them?

Well actually, this isn’t irrational buoyance. There are solid reasons why SaaS organizations have high valuations. The valuations are a consequence of the superior SaaS business model.

The market environment has changed; customers want to lease rather than buy – CAPEX, and not OPEX. They want the suppleness to try SaaS and then leave them, expand them, or leave them – business agility supports SaaS rather than software purchases.

SaaS based organizations take multiple forms. Software as a Service (SaaS) organizations such as Salesforce, and Infrastructure as a Service (IaaS) organizations such as Amazon have seen the highest growth, but there are multiple other SaaS industries like telecom, Media like Netflix, Healthcare, and also the “wine of the month club.” Organizations with recurring subscription revenue are seen favorably by the markets.

SaaS offer convenience, flexibility, and less lock-in for clienteles. SaaS need less time and effort for implementation – decreasing both the cost and the time to value (TTV) for clienteles.

Clienteles see the benefits of SaaS generating market demand, which powers the accelerated growth of SaaS organizations.

Legacy product retailers have a benefit in their resources, partners and clienteles. It requires a disruptive offering to seize these clienteles from the stakeholders – a SaaS offering can offer that disruption with latest capabilities, delivery mechanisms and pricing models with greater flexibility for clienteles.

SaaS organizations structurally can deliver more rapid advances than product retailers. Latest capabilities can be provided in SaaS update with their customers profiting from the most recent innovations rapidly. The capability to offer new benefits faster to customers provides a competitive advantage to SaaS organizations.

These benefits allow SaaS organizations to enter markets that were dominated by companies with a product sale mentality and contend successfully. Organizations without a SaaS offering won’t get a seat at the table – SaaS is usually a prerequisite in new projects.

Investors looks for organizations that disrupt the status quo.

And investors adore growth. The median growth for SaaS organizations is over three times that of Software product organizations.

Steady growth in revenue is followed by a growth in organization’s value. SaaS is a disruptive paradigm which permits companies with a SaaS offering to grow briskly at the cost of the incumbents.

Investors understands that SaaS organizations are gaining market acceptance, and are preferred as well, in most industries (such as health care) and applications (such as CRM). Markets once not thought viable for SaaS subscriptions (such as ERP) are now witnessing high and growing demand. Investors wants to recognize the new leaders in these emerging organizations serving these new markets for their possibly high investment returns.

While initial SaaS revenues are less, compared to product sales, over the life of the client, the recurring SaaS revenue value is more than product sales. This higher customer value through a long term recurring revenue stream eventually leads to greater revenue for the organization.

Investors value organizations that are growing rapidly. High SaaS revenue growth is a resultant of expansion and maintenance of the customer base along with revenue from new clienteles. Software product organizations must add more clienteles each quarter to grow, while SaaS organizations just add customers on-top of the present base.

Investors see the rapid growth of SaaS organization’s valuations. For example, in the last five years, Salesforce, the principal cap SaaS stock’s share price increase has been over double than that of Microsoft, Oracle, or SAP, the three software organization with the maximum market value.

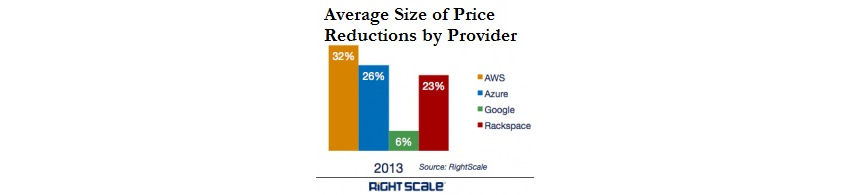

SaaS companies benefit from Moore’s law – their Cost of Service for the SaaS companies is decreasing year after year as public cloud costs fall. Amazon, Microsoft Azure, and Google have reduced the cost of their compute instances by 36% and their storage by 65% in 2014. Those SaaS companies that host their product in the public cloud saw their costs drop dramatically. Those who purchased servers did not.

The chart on the right shows the areas where aggressive competition have reduced hosting costs of SaaS companies in 2013.

Investors now understand how to assess SaaS finances beyond simple Income Statements. Investors look beyond the sold product sale based financial analysis to assess the SaaS vendor’s financial strength. They look at the value of the future revenue stream not included in the financial statements, not just the last quarter’s profit and loss, to assess the financial prospects of SaaS companies. The long term profit potential for fast growing SaaS companies is now well understood with more sophisticated analysis of the increases in the SaaS companies’ Customer Lifetime Value and cash flow.

Investors also highly value the long term revenue stability that a SaaS revenue stream provides.

SaaS companies have lower revenues than product sales companies marketing to the same companies with comparable solutions until the recurring revenue stream builds up to exceed the value of discrete sales. Product companies that shift to SaaS have reduced revenue and cash flows until sufficient SaaS revenue builds up to exceed that of their product sales. But investors now understand this and rewards the transition to SaaS even with a short term drop in profits and revenues.

Adobe transitioned its Creative Cloud Suite to a SaaS model in May of 2013. Despite an 8% decline of overall revenue, but with a near doubling of SaaS revenue, Adobe stock soared 55% in 2013.

Recent Posts

Categories

Archives

2014 © Confluo. ALL Rights Reserved. Privacy Policy